Industry Project

1. Supply Chain Finance Project for Yinan Yunqin Technology Company

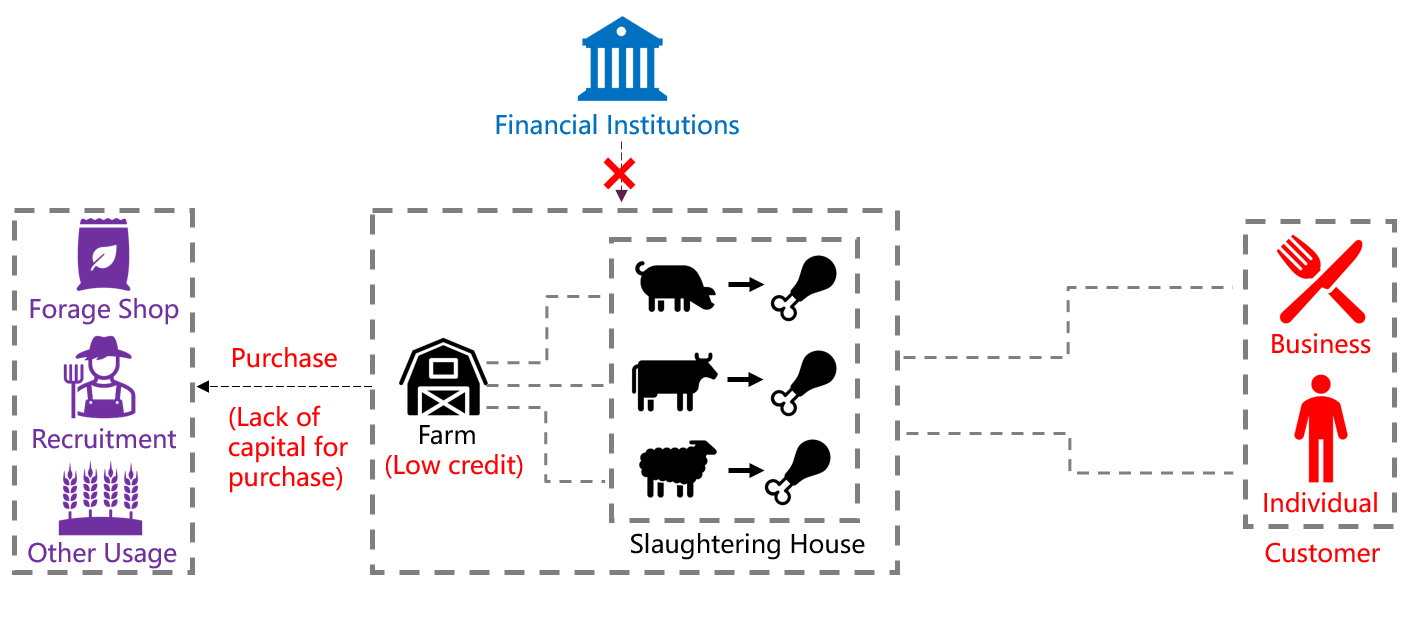

Background: With 25% of the country’s poultry production, Yinan County is regarded as the pillar county for national poultry processing in China. Yinan’s chattel supply chain presently contributes 70% of the county’s total GDP, which exceeds 2 billion dollars. However, many poultry companies in Yinan, particularly small and medium-sized companies like startup businesses, continue to grow slowly and consistently run into financial difficulties.

The primary cause of this funding shortage is the low credit of these startup poultry companies. Given the inadequacy of assessable assets and financing amount of these companies, financial institutions are less motivated to offer these businesses supply chain finance services because of a disproportion on their input and output efforts. Additionally, there are still many systemic problems and structural issues in the current guarantee systems, which are vulnerable in risk resistence when the bad loans of some start-ups emerge.

We, the Shenzhen Finance Institute (SFI) system analysis group, are fortunate to have been given the opportunity by the China Association of Small and Medium Enterprises (CASME) to provide the supply chain financial service for a startup company called Yinan Yunqin Technology Company to resolve their financial issues and construct a risk management information system for both Yunan and financial institutions to prevent the aforementioned credit risk.

Project Description: In this project, we establish the supply chain finance approach in two primary terms: chattel mortgage financing and accounts receivable financing, which make it easier for Yinan Yunqin Technology company to finance and reduce the potential risk of financial institutions at the same time.

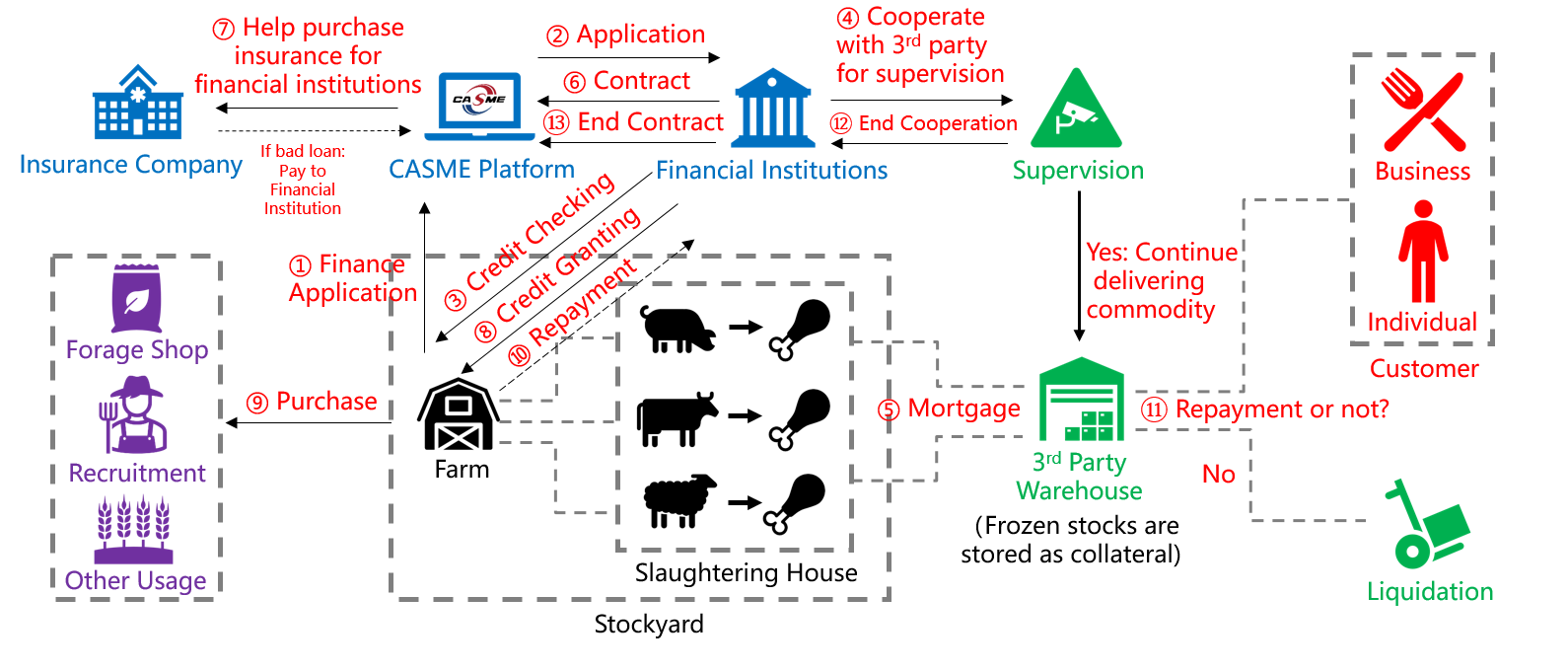

$\color{DarkGoldenRod}{(1)}$ Chattel Mortgage Financing: In the chattel mortgage financing service, when the Yunqin stockyard have a financial need, the financial institution can set the frozen stocks of the stockyard as mortgage in the third-party warehouse. The main steps of chattel mortgage financing are shown as follows,

Firstly, the stockyard makes finance applications to our CASME Platform for matching appropriate financial institutions $(①)$. Then, the CASME assists in matching financial institutions that are prepared to finance and introduces the primary financing process to the partner agency of the matched institutions $(②)$. After credit checking, the financial institution works along with a third-party warehouse that manages the stockyard’s mortgage until the financial contract expires $(③④)$. Following agreement, the stockyard is requested to give a mortgage for the same amount as the loan’s capital, which will be deposited in the warehouse until repayment $(⑤⑥)$. To entice more financial institutions to join this project, the CASME buys bad loan risk insurance for each financial institution enrolled in this platform. The insurance provider will reimburse the financial institution when a bad loan materializes $(⑦)$. Then, the financial institution provides the stockyard with funds so that the stockyard are capable to purchase necessary production materials $(⑧⑨)$. Ultimately, the stockyard pays off the loan and receives the mortgage before the deadline, and the financial institution cancels its agreement with the third-party warehouse and CASME. Otherwise, the financial institution can liquidate all of the mortgages $(⑩⑪⑫⑬)$.

A special case for chattel mortgage finance is Forage Finance shown in Figure 3. We encourage the financial institution to work with forage shops (or other similar businesses) so that financial institutions can directly finance stockyard forage instead of capital, in order to avoid the stockyard from claiming the value of loan capital consumption to exceed real credit. Through this approach, financial institutions would only be responsible for making repayments to the forage shop once the stockyard had declared their production-level requirements.

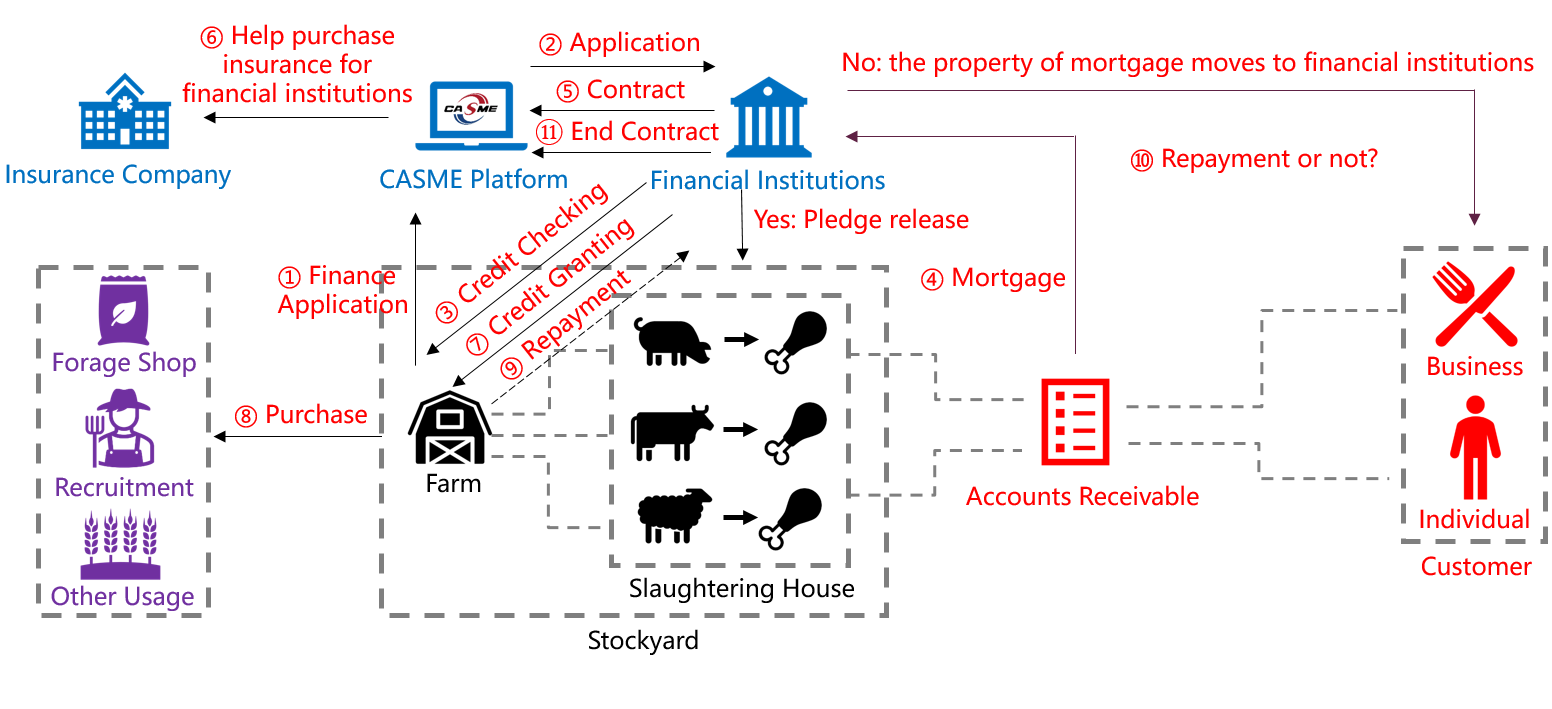

$\color{DarkGoldenRod}{(2)}$ Accounts Receivable Financing: Much like the chattel mortgage financing service, the accounts receivable financing service also provides stockyard financing solutions shown in Figure 4. In order to enhance the liquidity of mortgage, the collateral is changed from frozen inventories to accounts receivable of downstream clients. However, this service largely depends on the development and use of information accounting systems; otherwise, the operational risk of accounts receivable monitoring and retracing exists.

Even with the aforementioned supply chain finance approaches, this platform still faces some significant difficulties as shown in Figure 5. Firstly, it might be difficult for other supply chain participants to be aware of some existing transactions between different parties, so the information sharing is insufficient. Furthermore, it is also challenging to spot fraud since not all of the organizations disclose the transactions.

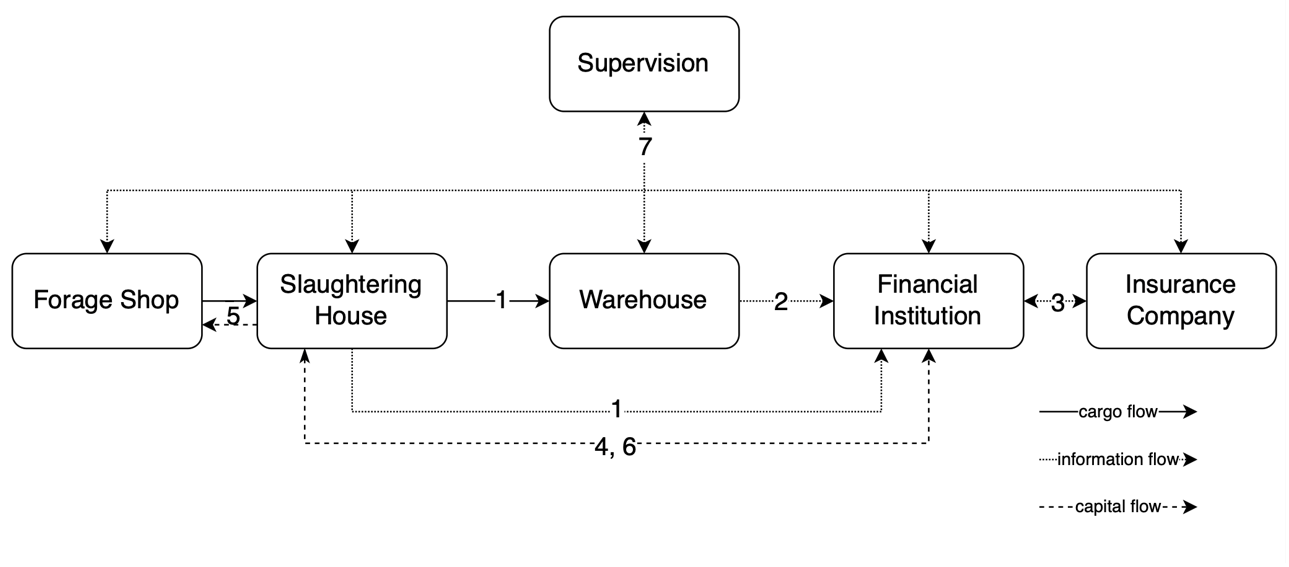

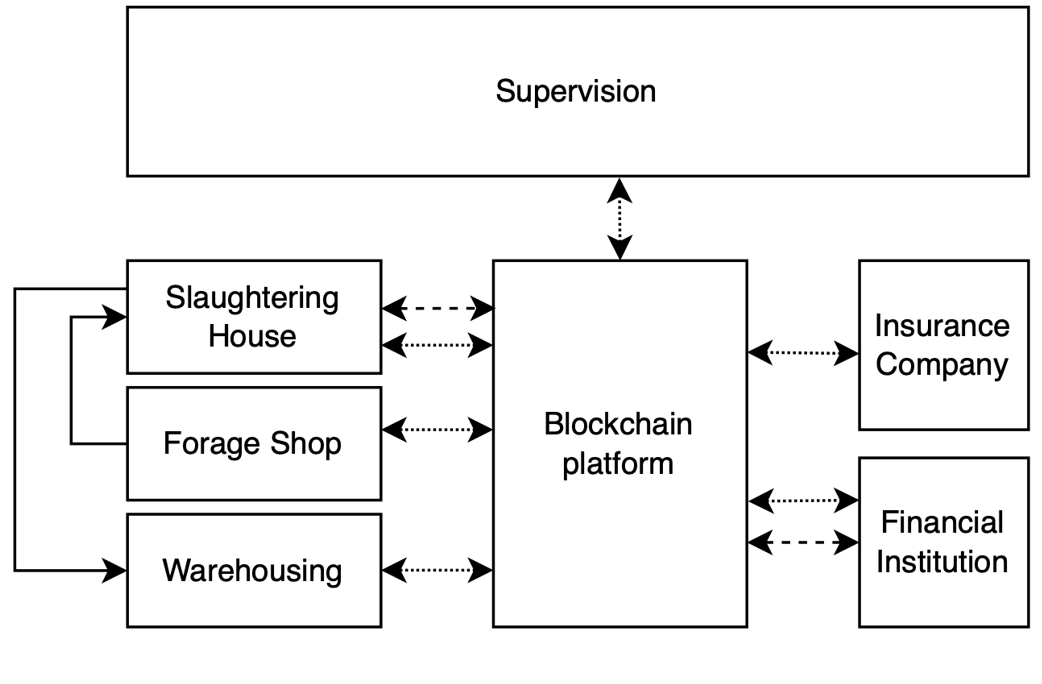

Therefore, an updated platform must be developed to enable transparency in data exchange and information sharing. Blockchain technology can be leveraged to create a supply chain financial platform to address the issue of insufficient data sharing. The blockchain’s distributed and decentralized characteristics facilitate audits and monitoring, and its immutability also aids financial institutions in risk management.

After integrating blockchain with the existing system, we can find several benefits from the information flow in Figure 6 and the issues we previously discussed can be resolved. Every transaction is recorded on the blockchain and is traceable since the blockchain platform receives all the transaction data. As a result, any companies can readily request access and query to all transaction records, which enhances the trust among all the parties. In the meanwhile, if any fraud or error occurs, all the information can be traced, allowing us to determine who should be held accountable.

Project Achievements: The main achievements of this project can be summarized as follows.

With blockchain technology, developed an integrated supply chain finance and risk management information system for YunQin and related upstream and downstream companies in the poultry supply chain, from which successfully managed financing transactions in a low risk way throughout the entire supply chain, including the electronization of accounts receivables, creditor’s rights, repayment, inventory management, etc.

Realized the synergistic benefits, information transparency and effective resource exchanges (more resources with more enterprises engaging in the future) among the poultry companies, suppliers, and financial institutions, which helped YunQin overcome its financial crisis and boost its overall profit by 65% over the first two quarters of 2021.

This project has been scored as 5.00/5.00 by the advisor Mr. Shen Zhenyuan from CASME.

I apologize for not disclosing all the details and information, particularly the information system part of this project, due to the CASME contract’s privacy requirements. If you are interested in this project, please also feel free to see here for an introductory system design [slides] and a brief summary [report] of our work.

2. AI-driven P2P Financial Risk Management Project of Lending Club

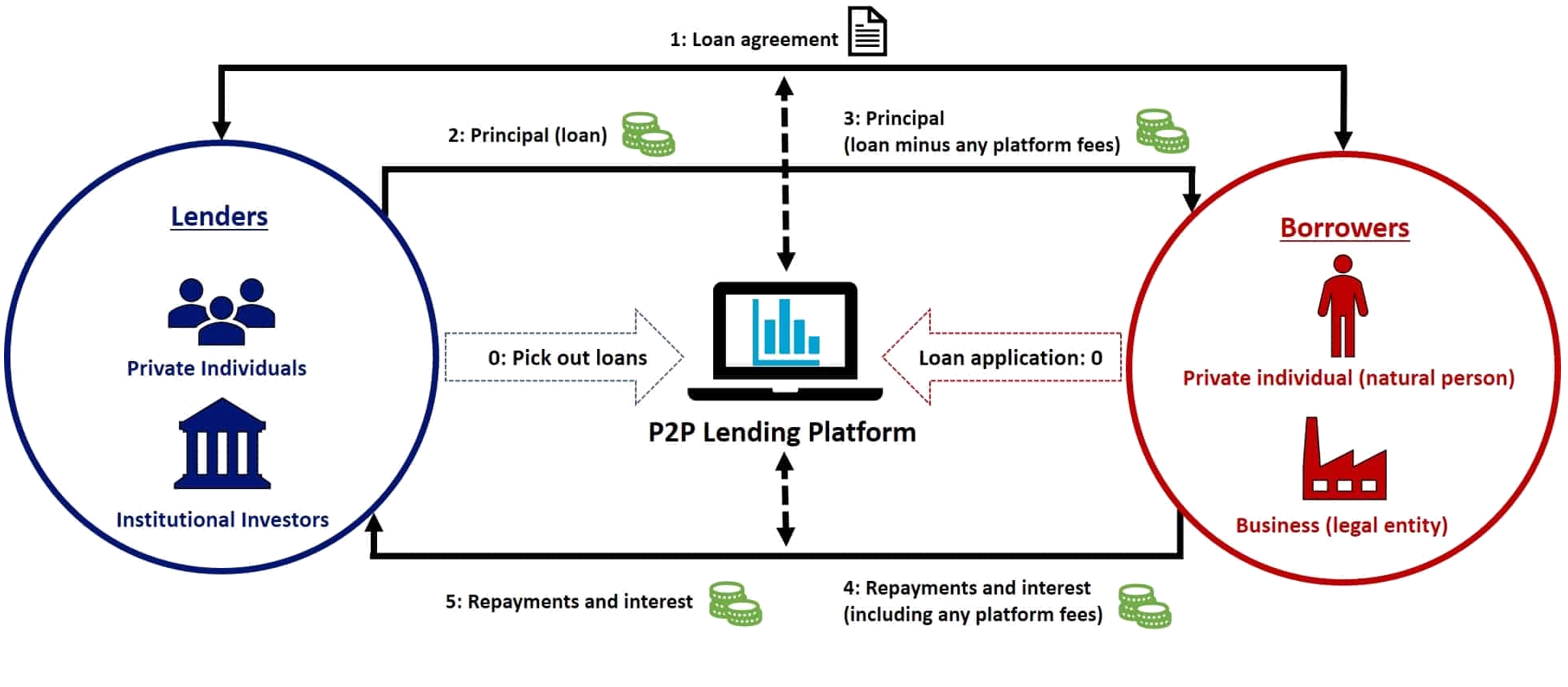

Background: Peer-to-peer lending (P2P) business, is a practice of lending money to individuals or businesses through online services that match lenders with borrowers. P2P lending company earns a profit from providing the match-making platform and setting interests.

However, the P2P business has encountered a significant number of defaulting cases from 2014 to 2019, which always causes serious financial catastrophes. The primary causes are the miscalculation of credits and the immaturity of the credit inquiry system. Even the world largest P2P company, the Lending Club, was not immune from this crisis. Lending Club provided us with information showing that, by the end of June 2018, there had been over 8500 cases of lending fraud reported. The related loss was over 800 million dollars, and the cases’ victims totaled over 2 million.

To address their issues with risk management, the Lending Club consulted the collaborative team from the Data Science and Information Technology Research Center of Tsinghua-Berkeley Shenzhen Institute (TBSI) and the Big Data Center of Ascending Powers Company, a data mining company dominated by the alumni of Tsinghua University. As the deep learning intern in the Big Data Research & Development Team of Ascending Powers, I’m fortunate to engage in this project and responsible for designing AI-driven financing and risk management approaches.

Project Description: In this project, the main challenges and flaws shown by the aforementioned fraud incidents for the Lending Club lie in 3 aspects: credit risk, mortgage risk, and account risk.

$\color{DarkGoldenRod}{(1)}$ Credit Risk: Even though Lending Club has developed a number of algorithms for calculating credit based on experience and machine learning, the majority of them are offline methods calculating massive data in a slow and ineffective way. Furthermore, despite the employment of these techniques, there is still a serious mismatch phenomena, in which many people and businesses with legitimate needs for financing are unable to do so because of “poor credit”, while others with problematic debts are still be granted with credit.

Additionally, the interest rates that are set and offered to borrowers are always based on experience, which shows a tendency to be overestimated. Due to the high interest rates, more current borrowers are defaulting on loans and fewer potential borrowers are attracted to take out loans on P2P platforms.

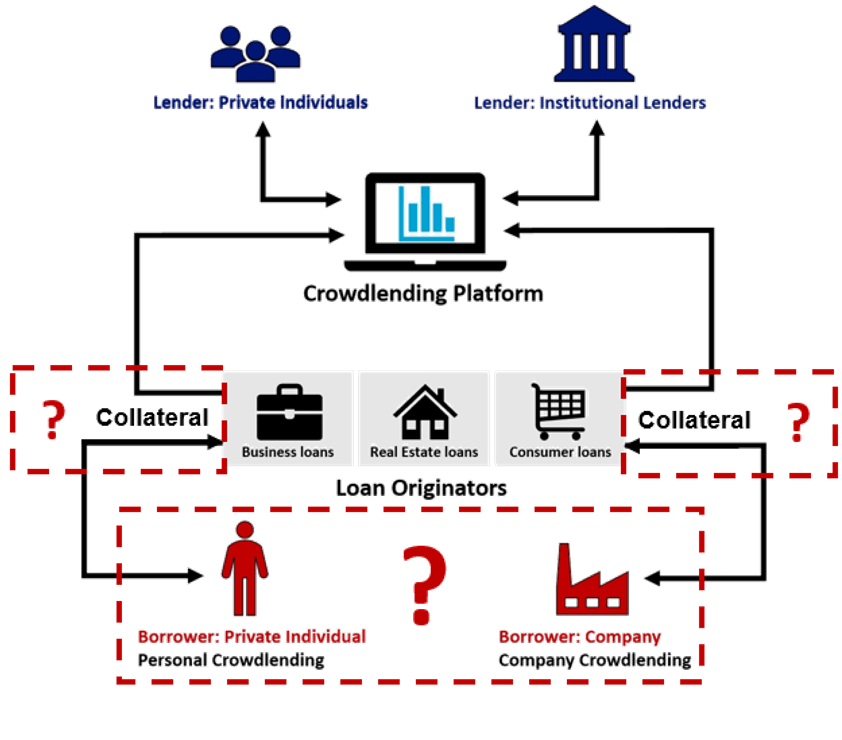

$\color{DarkGoldenRod}{(2)}$ Mortgage Risk: The mortgage risk is always encountered by Lending Club when making deals with supply chain related businesses or projects. As shown in Figure 2, the collaterals provided by crowdlending company borrowers may be subject to the risk of frequent variations in mortgage values, which might have an impact on the liquidation of the mortgage. Furthermore, inadequate inventory management would greatly increase the risk of mortgage deterioration, particularly for supply chains related to food and fruit.

$\color{DarkGoldenRod}{(3)}$ Account Risk: The account risk is severe when making deals with companies from traditional industries. Numerous traditional businesses still use paper bills or currency since informatization and electronization are not common in those industries, which leaves room for many businesses to make counterfeits. From 80% of the Lending Club fraud cases where accounts receivable were used as collateral, the untraceability of these debts comes from the fact that part of the account receivables are bad debts and the rest of those are sourced from fictitious firms or corporations that have been written off.

To resolve the above risks, we mainly focus on the modification of current credit investigation system in terms of 3 aspects: clients grading, loans judgement, and intelligent interest rate setting.

$\color{DarkGoldenRod}{(1)}$ Clients Grading: The current approach either solely uses loan history to arbitrarily determine creditworthiness or treats every borrower as a new client, feeding data directly into neural-nets models without taking into account the interpretation of clients. However, 36% of the clients signed up for Lending Club without having a loan history over the previous five years, which results in a great erroneous judgement for new clients - also the main task we predominate in for client grading. After appropriate feature engineering, we collected 200+ client related features including salary, region, accumulated loan amount, etc. Then, we used multiple-means type clustering methods on these features to create clusters and then explained these clusters to create client portraits, which can also be used as a key feature in loan judgements and assist those in charge of setting interest rates in better interpreting clients, whether in an automated or manual manner.

$\color{DarkGoldenRod}{(2)}$ Loans judgement: Based on the Lending Club’s current algorithms, we ameliorated the training process of data mining by shifting current offline platform to an online co-training AI platform with more stochastic algorithms involved, which also resolved the aforementioned new client problem. The term “Co-training” refers to a training approach that enables the online training of several parties using distributed devices, protecting data privacy while enhancing training effectiveness using numerous delicate Few-Shot Learning (FSL) techniques. After numerous iterations of online distributed FSL data mining, as shown in Figure 3, the generated demo versions are integrated to make adversarial trainings in the co-training AI platform, from which the customized AI-driven loan judgement product was derived. In comparison to the previous AI training process, our online co-training AI scheme greatly improved the data utilization and accelerated the training process through online FSL training under high data security.

$\color{DarkGoldenRod}{(3)}$ Intelligent interest rate setting: Due to the subjectivity of manual interest rate setting, we developed an intelligent system that automatically generates reference interest rates to assist interest rate setters. After removing the loan data that was significantly impacted by macroeconomic factors, such as the P2P financial crisis, we chose the data of clients who are considered to have a high risk of defaulting on loans or who have a history of defaulting on loans with other financial institutions, but who have never defaulted and have a high second visit rate with Lending Club. Also, the chosen data are situated in a time where the number of clients has significantly increased. Then, we regarded the chosen interest rate as relatively reasonable and rational, and set it as predictor to train on our AI platform to develop a customized AI product for determining interest rates. Fortunately, compared to the previous 5 years, the interest rate set by the intelligent system has lowered by 35% in average, and more new clients are therefore involved.

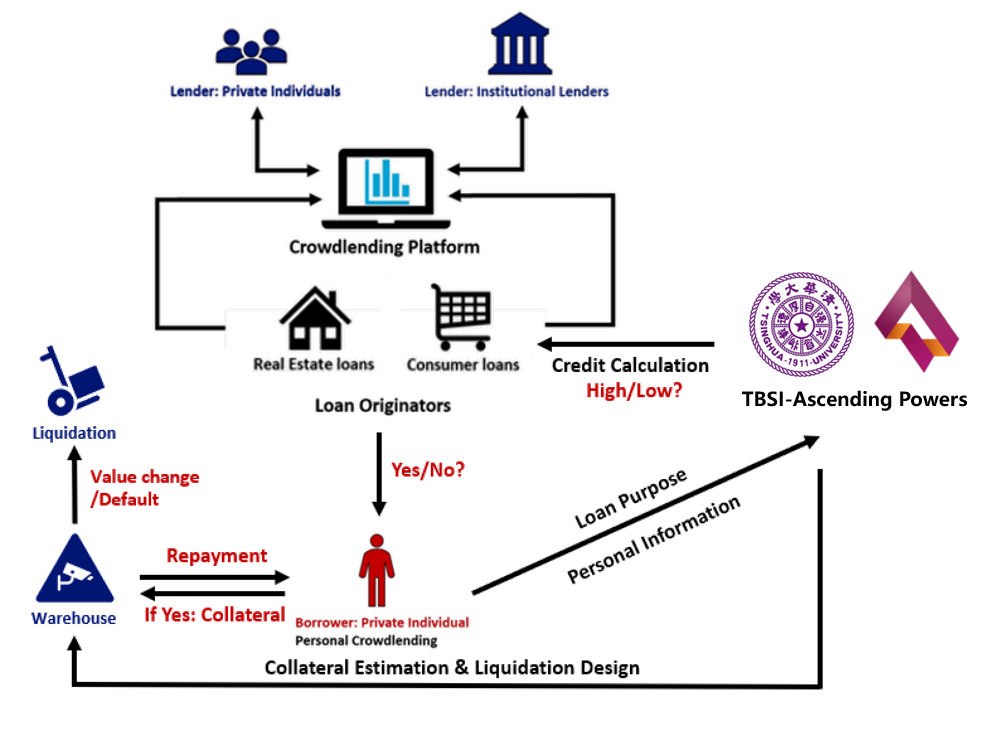

Through our modification on the current credit investigation system, the credit risk of the Lending Club has been greatly decreased. Similiar supply chain financing strategies that I described in the previous Supply Chain Finance Project for Yinan Yunqin Technology Company can be used to address the mortgage risk and account risk, as illustrated in Figure 4.

Project Achievements: The main achievements of this project can be summarized as follows.

Identified the main credit issue for Lending Club, the new client judgement, and successfully resolved it through client grading and loan judgement. Also successfully addressed the mortgage and account risk by mature supply chain financing strategy and built the first intelligent interest rate setting system semi-automatically applied in P2P industry.

Avoid using massive data blindly and neural-net models without interpretation; instead, implemented some most recent research achievements like FSL and online co-training AI platforms, which significantly reduced the sample size requirements, improved data utilization, and accelerated training process while maintaining high data security.

After applying our AI-driven loan financing strategy, the Lending Club was able to cut its bad loan rate by 48% in 2020 compared to the previous year.

I have to apologize again for not revealing all the information of this project for the same privacy issue as I claimed in the previous Supply Chain Finance Project for Yinan Yunqin Technology Company. But I wrote a reference [codes] that outlines the brief idea of this project employed in other loan prediction cases, hope this code can help for better understanding.